CS4246 Cheatsheet

Problem Specification

- Initial State

- Possible Actions Action(s)

- Transition Model Result(s,a)

- Goal Test

- Path Cost c(s,a,s')

- Admissible Heuristic: Never overestimate cost to goal

- Consistent / Monotonic: Straight path (to goal) always shorter than a curved path.

- Factored Representation: State representeed as SAT

- Fluents: state variables in said representation

STRIPS

- Problem spec: Initial State, Actions, Result, Goal

- Action: Action(params),

- Precond: Descript

- Effect: Descript

- Negation (Delete list), otherwise Add List

- Goal: Partial state, must be fulfilled

- Action: Action(params),

- State: +ve literals ANDed together with no unknown variables or functions.

- Negation not allowed (use literals that are negative)

- If literal not specified in state, it is false (database semantics)

- Search:

- Forward: wk 1 39/65

- Backward: wk 1 40/65

- Relevant-state search:

- Actions are relevant when:

- Action doesn't negate a predicate in the current goal

- Action unifies a predicate in the current goal

- Add the preconditions of the action to current goal descript

- Actions are relevant when:

- Relevant-state search:

- Heuristics:

- Ignore preconditions

- Ignore delete lists

- Assume subgoal independence, decompose problem

- Turning into SAT problem

- Complete the initial state by adding negations to omitted ground literals

- Complete the goal by taking every possible grounded combination of the goal and ORing them together.

- e.g. ...

- Axioms

- successor-state:

- Solves Frame problem (most actions don't change fluents) 60/65

- Pre-condition: Action taken at time => Precondition was true

- Action Exclusion: both actions cannot be taken at same time step.

- Not (Action1 at t) v Not (Action2 at v)

- successor-state:

Utility Theory

- Axiomatic approach, assume agent has consistent preferences for outcomes (GT >, LT <, EQ ~). Represented as U(Outcome).

- Utility can be preserved with monotonically increasing transformation.

- Axioms

- Orderability / Completeness: For any 2 outcomes, only 1 preference (agent prefers one, or both equal)

- Transitivity: (A > B) /\ (B > C) => (A > C). Otherwise irrational

- Continuity: If 3 outcomes: A > B > C where B is sandwiched. Then there must be a p where agent always get B, then A with probability p or C with probability (1 - p).

- Lotteries: [p1, O1; p2, O2...] Probability p1 for outcome O1 etc

- Susbstitutability: If A ~ B, then they can be swapped within a lottery

- Monotonicity: If A > B, then agent must prefer A.

- Decomposibility: 16/52 Chained lotteries can be reduced to simpler ones

- Expectations:

- Expected U(outcome): All probabilities x outcomes

- Principle of Maximum Expected Utility (MEU)

- Rational agents must maximize expected utility

- Expected Monetary Value (EMV): wk1, 28/52

- Risk-neutral: montonically increasing, line up

- Risk-averse: Log of money amount.

- Risk-seeking: U(L) is more than the straight line later on

- Certainty Equivalent: Value agent will accept in lieu of a lottery

- Risk Premium: EMV - certainty equiv

- Normative theory: how agents should act

- Descriptive theory: how they actually act

- Irrationalities: Ambiguity aversion, framing effect, anchoring effect (35/52)

- Optimizer's curse: 36/52

- Bayesian and Decision networks 40/52

- Given observed outcomes, calculate probability of affected outcomes

- Chain rule

- calculate expected outcome value based on these probabilities

- Value of Perfect Information VPI

- Given this new information, calculate new expected outcome

- Split into cases (See 47/52)

- Pr(info success) x Pr(success)

- Pr(info fail) x Pr(fail)

- VPI = new outcome - old outcome

- Split into cases (See 47/52)

- Non-negative expected value

- Not additive with other VPIs

- Given this new information, calculate new expected outcome

MDP

Principle of Optimality: A value of a state is its reward + best future rewards from state. 20/54

Online Search 39/54

- Handling curse of dimensionality with MDPs

- Imagine it as a tree

- Nodes: values , Edges: transitions

- Tree size:

- Sparse Sampling: Don't check future for some states

- Rollout: Simulate many trajectories from a state to estimate action with best returns

- Monte Carlo Tree Search: 43/54

- Selection: Dig down the tree until depth reached or node not simulated yet

- GLIE. Explore first, then become more greedy (Decrease epsilon as time goes on).

- Expansion: If state not terminal, Create child nodes from this state.

- Simulation: Choose one of the child nodes,C, and do random rollout.

- Backpropagation: Propagate the reesult of the rollout to update node values from C to root.

- Selection: Dig down the tree until depth reached or node not simulated yet

- Upper Confidence Tree (UCT) 48/54

- A strategy for selecting a node for MCTS

- Choose action that optimizes (current estimate + exploration * sqrt(ln(times node visited) / ln(times node visited and took action a))

- Balance expected value and exploration

Bellman Eqn 21/54

Evaluate policy using dynamic programming

Value Evaluation: Init V = 0

:

:

:

- (s): state, (s,a): action, (s,a,s'): transition

Value Iteration: Given model (R, A, T(s,a,s')), recurse bellman until all converge

Policy Iteration: Init V = 0, = random

- Evaluate based on , not max (using bellman)

- Update if V for any action <

- Stop when no change / horizon reached

Prediction: Evaluate a given policy, Control: Find optimal policy

Model-Based, Adaptive Dynamic Programming Agent: Iteratively given observations, construct R and T(s,a,s'):

- R: = observed R(s). In addition, U(s) = R(s) when a new R(s) is observed

- T(s,a,s'): (times transition observed) / (times action at state)

- these variables are tracked with a table

- Prediction: Update U using Policy-Evaluation after each observation

- Control: Update U using Policy-Iteration after each observation

-greedy: action = (1-e)(best) and (e)(random)

Greedy in the Limit of Infinite Exploration (GLIE),

Monte Carlo Learning (Direct Utility Estimation): of rewards from s to end]

- = of rewards from s to end

- i-th episode, k episodes thus far

- Concept: [(New Info) - (Current Estimate)]

- New Info = Target, Difference = Error

- equals equals

- Monte Carlo Target:

- Monte Carlo Error (converges to 0 when k = ):

- Prediction: Calculating V(s) is enough

- Control: Calculate , then update by

- = of rewards from s to end

Temporal Difference Learning (TD(0)): Same as MC Learning but estimate with every step in the episode instead.

- Change the target:

- $ = V{k[j+1]}(s) = V{k[j]}(s) + \alpha(R{k[j+1]}(s) + \gamma V{k[j]}(s') - V_{k[j]}(s))$

- k episodes thus far, j-th step in the kth episode

- TD Target:

- Converges faster but biased

- SARSA: TD(0) using 1 for generating data and training(on-policy)

- State-action-reward-state-action: algo for learning MDP

- Future value estimate by action taken by

- Target:

- on-policy converges if -greedy

- Q-Learning: TD(0) using 2 : 1 for generating data, 1 training (off-policy)

- Future value estimate by best action based on current estimates

- Target:

- off-policy converges if decays and all transitions taken infinitely times

n-step TD (TD(n)): Somewhere between TD & MC: Change target to combine future steps in 1 update

- 0-step (): TD target =

- 1-step (): TD target =

- 2-step (): TD target =

TD(): n = , = 0 to 1, weight and normalize by geometric progression

- : New observed V(s) given n-step estimation

- Conceptually, All are estimations of the same thing, hence the eqn =

- Using Geom Progression:

- Hence

- Computation:

- Eligibility trace : track how "fresh" each state is by frequency and last visit

- Init = 0

- Types:

- Accumulating : += 1 if state visited at step

- Replacing : = 1 if state visited at step

- "Decaying Effect": With every timestep,

- Eligibility trace : track how "fresh" each state is by frequency and last visit

- Using eligibility traces, and timestep, update V(s). The TD error is weighted by each state's own eligibility trace.

- timestep, update all eligibility traces:

eligibility *= lambda * gammaeligibility[state] += 1.0

- Then get the TD error for the current timestep:

td_error = reward + gamma * state_values[new_state] - state_values[state] - Then finally update U(s) for all states:

state_values = state_values + alpha * td_error * eligibility

Function Approximation

- State space too large, approximate with a linear function that takes in a vector of params :

-

- Multi-variate s: , where s=(x,y)

- : Can approximate by:

- Keep a constant, then estimate using 1 linear fx per s

- Use a single linear fx that accepts s and a as params

- Supervised Learning

- Learn using initial training sample set

- Do least squares estimation to fit params

- e.g. given linear function

- you have a set of samples where V is value of the linear function and x and y are the function input, do linear regression to solve

- Online Learning

- Use gradient descent to minimize Error(s) (MC Error, TD Error etc) by modifying params on every observation

- Error(s) = (approximated_V(s)) - (observed_V(s))

- "approximated_V(s)" is

- observed_V(s) - approximated_V(s)

- : differentiate linear function w.r.t.

- You can swap out the error portion in the assignment above with any of these:

- Monte Carlo Error: (approximated_V(s)) - (observed_V(s))

- Semi-gradient methods (target biased as it depends on ):

- TD Error:

- Q-Learning "Error":

- Deadly Triad: Sources of instability

- Function Approximation

- Bootstrapping: Use current estimates as targets, e.g. TD Rather than complete returns, e.g. MC

- Off-policy: Training on transitions other than that produced by the target policy.

Deep Q-Learning: Q-learning with non-linear function approximation

- Use experience replay with fixed Q-targets to make inputs less correlated & reduce instability

- The procedure below uses double Q-learning

- Procedure:

- Take ϵ-greedy action using approximated policy from main policy_NN

- Store observed transition in a round-robin buffer

- Repeat until transitions, then loop times:

- Sample random mini-batch of transitions from buffer. Do the following as a batch:

- Compute based on actions policy_NN took to produce the transition

- Compute

- Compute by

- Compute Huber loss between and

- Gradient step on loss

- Increment episode count

- Set target_NN's params to main_NN's params after every C episodes

- Reset environment, update and repeat from step 1

Policy Search

- See other document.

POMDP

- Updating belief' given (b, a, e)

- Set initial belief (set of probabilities of being in each state)

- Do action: next_state, all Pr(you were in prev_state) x Pr(transit)

- Use evidence: state, x Pr(evidence seen at state)

- Normalize s.t. all state beliefs = 1

- Value () of plan with n steps

- Recursively "unpack" future rewards as necessary

- Evaluate E[value] after executing plan from

- Plan: Pre-planned sequence of steps

- Optimal Plan:

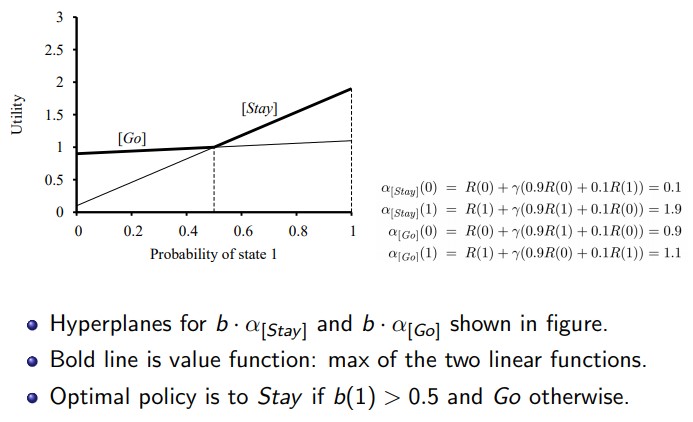

- x-axis: Pr() (0-1), y-axis: value )

- Plot: All possible values of plans w.r.t. Pr(s) (). Each plan is a line formed by 2 points:

- Point 1 at x-axis 0:

- Point 2 at x-axis 1:

- Optimal: Switch between plans that offers highest given regions of Pr()

- POMDP Value Iteration: Keep calculating plans while removing dominated plans. If no change after awhile, then return set of dominating plans.